According to the “Rule of Three” in business and economics, all major

industry sectors, no matter how fragmented, ultimately coalesce such

that no more than three full-line generalist mega players together

dominate the market. Most healthcare provider markets today are moving

in that direction; some are already there. But the most dramatic

changes are still to come.

In recent years, a steady flow of mergers, acquisitions, joint ventures and strategic alliances has transformed healthcare markets across the country, giving rise to health networks that continue to grow in size, geographic reach and economic power.

While this consolidation process continues to play out differently by region, the first tipping point is already behind us. By 2020, most markets will be dominated by two or three major health networks. Tomorrow’s health network will serve a population spread out across multiple population centers—even multiple states—and connect with patients at every point along the care continuum, from prenatal care to hospice care.

To date, health network growth has been primarily horizontal and focused on adding more beds, physicians and patients. The largest health networks are already approaching the regulatory limits of market share growth and shifting their focus to vertical integration—post-acute care, retail and digital health, and insurance. Of course, new constructs bring new challenges—mission dissonance, increased capital demands, unfamiliar skill set requirements and heightened political scrutiny.

These changes are occurring rapidly, impacting costs, outcomes, the competitive environment and the way patients access healthcare. A decade ago there were many markets in which no single hospital system had more than 15% market share—even when narrowly defined by inpatient admissions. In 35 of the 50 largest metropolitan areas in the United States today, the three largest health networks represent more than two-thirds of the market. These are multibillion-dollar healthcare conglomerates that collectively drive the way in which care is delivered to their communities. (See Exhibit 1.)

From Cottage Industry to Conglomerates

The U.S. healthcare economy is about $3 trillion annually; in GDP terms it would represent the fifth-largest economy in the world. The provider sector is the largest slice of the U.S. healthcare economy and, given its sheer size and significance, its transformation has implications that are at once uniquely far-reaching and deeply personal. The provider sector has historically functioned as a cottage industry—hands-on and locally based. There have been other periods over the past few decades when massive provider consolidation has seemed imminent, but prevailing fee-for-service reimbursement models and protectionist regulatory mandates have always served to maintain the status quo. Today, the industry’s appetite for partnerships, affiliations, mergers and acquisitions is primarily rooted in the payment emphasis shifting from volume to value. Reimbursement per unit of care is declining, making traditional payment models less and less tenable. Fee-for-service is steadily giving way to population health payment models, requiring a level of clinical integration and business intelligence that independent entities find difficult to create.

Also, as payers push back on annual provider rate increases and increasingly link payment to value and outcomes, more and more of the payment burden is being pushed onto patients, who have an increasingly powerful incentive to participate actively in their own healthcare choices and shop for the best value. If you believe that incentives drive behavior, then a 180-degree flip of the reimbursement environment is convincing evidence that the provider sector is unlikely to slip back into the fragmented state of the past three decades.

In the provider sector, as in most industries, the calculus of consolidation is simple and straightforward: A market share below 10% is not economically sustainable; a market share above 50% becomes anti-competitive. Over time, the market achieves balance with two or three major players, each with a share between 10% and 50%.

There were 100 hospital mergers and acquisitions in 2014, double the 2005 tally, according to Irving Levin Associates.ii (See Exhibit 2.) Hospitals large enough to remain independent in the first wave of consolidation are now determining that it is time to join the party. The shakeout has already reshaped the contours of healthcare delivery in most markets. A 2013 study by the Alliance for Health Reform found that 78% of U.S. hospitals were either considering or carrying out a merger.

This is not to suggest that the pace of change will be the same from market to market or that every independent hospital is doomed to financial difficulty and eventual consolidation. Even in highly consolidated markets,

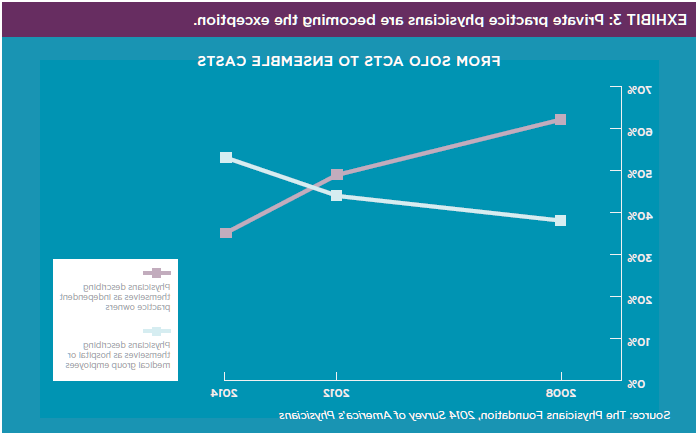

the Rule of Three predicts there will always be a place for specialist providers—freestanding children’s hospitals and freestanding cancer centers are among the most financially robust members of the provider sector. And some independent providers (hospitals and physicians) are coming up with novel ways to remain independent (e.g., via concierge practices). But going down the street to see the friendly primary care physician with her own shingle or being admitted to the local independent hospital for surgery will increasingly be the exception rather than the rule, as illustrated in Exhibits 3 and 4.

Pushing Against the Boundaries

The horizontal expansion of provider networks has historically been constrained by patients’ unwillingness to travel beyond a certain distance for care and the inability of networks to track their patients’ care once they’ve left the system. But large networks have become much more adept at distributing clinical services appropriately across a broad region and tracking the care delivered across the continuum—all with a focus of providing appropriate care in the appropriate location for the appropriate cost. For example, most of northeast Ohio has now consolidated into one of two health networks—University Hospitals and Cleveland Clinic. With limited opportunity to further expand within the metro Cleveland market, the latter expanded southward by acquiring a stake in Akron General Health System.iv And the merger of Hackensack University Health Network and Meridian Health creates a supersized healthcare network that links north and central New Jersey and covers fully two-thirds of the state.v

Where a healthcare network’s target service area once aligned with metropolitan statistical areas (MSAs), now it is increasingly spread out across an entire state. We are beginning to see some of the largest provider networks—particularly national for-profit systems and some faith-based institutions—routinely target out-of-state acquisitions, redefining “market” in terms of regions rather than single population centers.

As they reach the limits of horizontal consolidation within a given population center, these networks are also facing intensified scrutiny by state and federal regulators. Invoking the 1914 Clayton Antitrust Act, the Federal Trade Commission has successfully challenged proposed hospital mergers in Georgia, Illinois and Ohio over the past two years on the grounds that they would raise prices and suppress competition.vi In another high-profile case, the Massachusetts attorney general initially allowed Partners HealthCare—the largest provider in the state—to proceed with its planned purchase of two in-state systems on the condition that any price increases not exceed the rate of general inflation for six years. Despite the agreement, the deal met with vigorous opposition from other entities across the state, and Partners ultimately was forced to reverse course.vii

Expansion-oriented networks are pushing back hard against regulatory restrictions.

But as the avenues to horizontal integration narrow, these multibillion-dollar conglomerates are increasingly considering vertical integration plays, including expansion into pre- and post-acute care entities and investments in new technology and digital health. Today, 60% of family doctors and pediatricians, 50% of general surgeons, and 25% of surgical subspecialists are salaried employees, according to the American Medical Association.viii There has been a rash of post-acute care partnerships and acquisitions in the past two years and even increased expansion into a sector that has historically been beyond the scope of most healthcare providers—insurance. Many of the country’s largest provider systems—including Sutter Health in California, Denver-based Catholic Health Initiatives and St. Louis–based Ascension Health—are moving upstream into insurance to try to capture the value associated with better management of patient care.ix

The impact of all this consolidation on clinical outcomes and patient premiums is still being debated, and challenges are likely—from regulators as well as the insurance industry—but the integration of the provider and insurance sectors seems to be accelerating. Needless to say, the skill sets required to calculate and manage the actuarial risk of a patient population are dramatically different from those required to deliver clinical care, and some hospitals will invest heavily in the effort only to fail. But those who succeed will be in a position to capture the value of cost efficiencies and economies of scale, rather than sign that value over to insurance companies.

Healthcare Consolidation: Envisioning the Next Wave

In a remarkably short period, horizontal consolidation has reshaped the U.S. healthcare provider sector, forcing all stakeholders to rethink once-axiomatic assumptions about the way healthcare should be accessed, delivered, evaluated and priced. But consolidation is a process, not an endpoint. As networks continue to test the bounds of horizontal expansion while experimenting with vertical expansion, a third dynamic could unravel all of the consolidation activity of the past few years.

When industry consolidation does not result in meaningful improvements in value to the end-user, entrenched players become attractive targets for disrupters.

While proponents of market consolidation say it will ultimately enhance the quality of care, remove waste and bend the cost curve, there is now growing evidence that the benefits of consolidation are not accruing to the patient. Several studies suggest that consolidation is actually having the opposite effect—lessening competition, providing the clout necessary to raise prices and creating “too-big-to-fail” healthcare networks for which the traditional market-based checks and balances no longer apply. When a network represents more than a third of the healthcare delivered in a market, there is a sense that it is irreplaceable—even in the event of catastrophic financial losses or egregious medical negligence.

Here too the provider sector can take a lesson from how the Rule of Three has played out in other industry sectors. When industry consolidation does not result in meaningful improvements in value to the end-user, entrenched players become attractive targets for disrupters. And with the size of the healthcare provider sector, there will be no shortage of interested parties. We are already witnessing a boom in the number of potential disrupters—and these aren’t limited to the garden-variety startups common to smaller sectors.

In the past 12 months, a host of Fortune 100 companies have trained their sights on the provider sector—from the repositioning of CVS Health to announcements from Apple, Google and Walmart of major healthcare initiatives.

The consolidated healthcare network being created in many markets, with the hospital at the center, may have a remarkably short shelf life; the onus is on the provider sector to prove the juice is worth the consolidation squeeze.

Published December 1, 2015